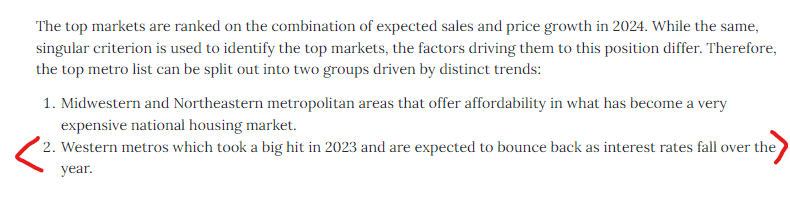

We’re in the forecasting time of year!

The chart above is from Realtor.com. We are used to the ivory-tower types who don’t bother to get out of their office or even pick up a phone. They just shine up their previous guess with some current events, like lower mortgage rates, and tell everyone we’re going to be fine.

But their guess that sales will be up 11% in San Diego is preposterious, and giving credit to lower rates doesn’t address the ultra-low inventory that is so likely to persist:

For sales to increase by 11% means that inventory will have to increase by the same or higher amount. While an 11% to 20% increase in the number of homes for sale would be fantastic for the market, there is virtually no evidence to support that idea – other than I have three listings booked already.

https://www.realtor.com/research/top-housing-markets-2024/

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

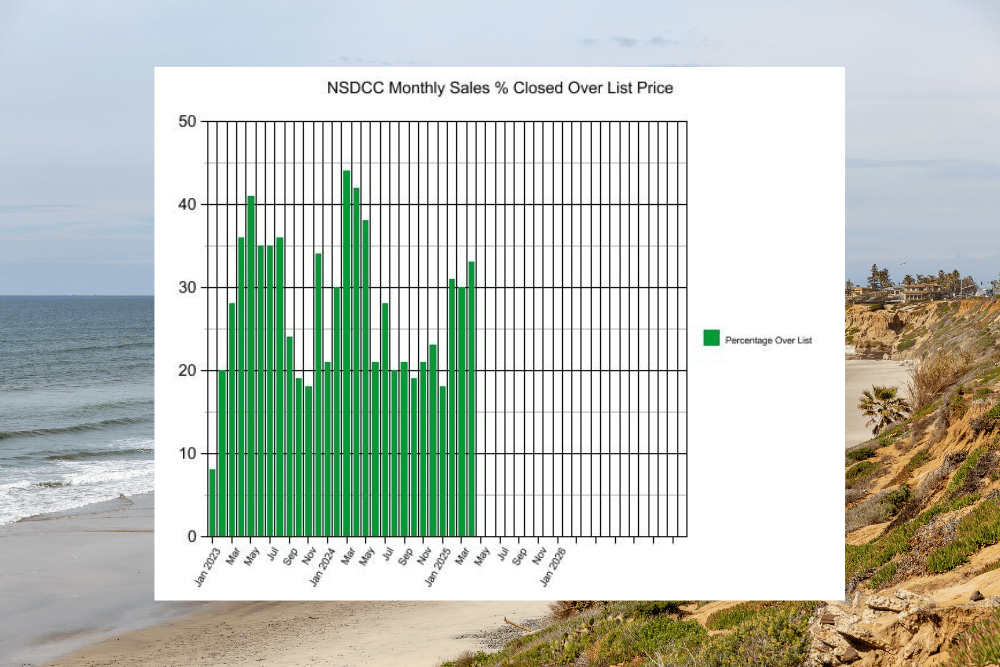

If you’d like to make your own predictions, here is some local data (La Jolla to Carlsbad):

NSDCC Detached-Home Listings & Sales, Jan 1 to Nov 30

I’m guessing that sales will be flat/same in 2024, and the median sales price will be +4%.

Why? Because I think we’ll see mortgage rates in the sixes, which will help to energize the demand. The number of listings may grow slightly but not up by more than +10% and many will be wronger on price, which will cause the number of sales to be about the same as they were in 2023.

We know it will be hot during the selling season, it’s what happens in the second half of the year that will drag down the median sales price.

Here’s what I thought last December.

More Predictions

Lawrence Yun, NAR’s chief economist, believes mortgage rates could remain around 7 percent for most of 2024. However, he thinks rates have likely crested: “I believe we’ve already reached the peak in terms of interest rates.”. Within two years, he says, the rate should return to 5.5 or 6 percent.

Yun foresees no major changes in purchase price tags on a nationwide level next year, with fluctuations of only about 5 percent one way or the other. The only exception is California, he says, where the market could see 10 percent declines: “Because it’s so expensive, California is always the most vulnerable to changes in interest rates.” Overall, in five years, Yun expects prices to have appreciated a total of 15–25%.

McBride predicts home prices will average low- to mid-single-digit annual appreciation over the next five years. This rate of appreciation, he says, is consistent with the long-term average of home prices increasing by a rate that hovers a percentage point above the inflation rate.

While it may show bubble-like characteristics, Yun does not expect the residential real estate market to pop. He said, “A crash happens with oversupply,” Yun says. “A 30 percent decrease will not happen, because there isn’t enough inventory.” He believes the housing supply will balance out within five years.

Zillow has a similar forecast, as it expects home values to rise by 6.5% from July 2023 through July 2024, despite “despite persistent affordability challenges.”

Likewise, Freddie Mac is forecasting prices rising by 0.8% between August 2023 and August 2024, followed by another 0.9% gain in the following 12 months. Part of the rebound in prices is based on the “large cohort of Millennial first-time homebuyers reaching prime home-buying age,” Freddie Mac reports.

The CoreLogic HPI Forecast indicates that home prices will not change on a month-over-month basis (0.0%) from October 2023 to November 2023 and increase on a year-over-year basis by 2.9% from October 2023 to October 2024.

Rick Sharga said, “Home prices will probably rise slightly in 2024, perhaps by 2-3% as demand continues to outpace supply. However, this will not be universally true; some formerly high-flying markets like the Bay Area in California, Austin, and Phoenix could see prices continue to fall, while cities in the Southeastern states may see prices rise more quickly.”

Nick Ron, founder and CEO of House Buyers of America, expects average home prices in the U.S. to rise around 3 to 4% next year. “But at some point in 2024, I see a slowdown in price growth.”

Goldman Sachs analysts predict home prices will continue to climb before dipping this winter, then rebounding “only modestly” in 2024. Then, their model projects “a rebound to below-trend home price growth … as rates decline modestly but remain at elevated levels.” In December 2024, they predict national home prices will increase by 1.3% year over year. That’s a downward revision from July, when Goldman predicted a 1.7% home price increase in 2024. So far in 2023, home prices have increased an estimated 4.2% “but are likely to fall 0.8% through December for a 3.4% year over year increase,” Goldman analysts wrote.

Not all forecasts expect home prices to climb, however.

Redfin thinks that home prices will fall 1% year over year in the second and third quarters, when the home-selling season is in full swing. That will mark the first time prices have declined since 2012, when the housing market was recovering from the Great Recession, with the exception of a brief period in the first half of 2023.

Based on declining affordability and more homes being built, both Moody’s Analytics and Morgan Stanley expect home prices to fall slightly in 2024.

Morgan Stanley housing analysts expect home prices to hold steady year over year in 2023, before edging lower next year.? “We forecast house prices in 2023 to finish the year flat versus 2022 before falling 2% in 2024 as affordability continues to adjust slowly back to long-run averages and inventories begin a slow climb off multi-decade lows,” wrote the firm’s housing research team.?

Moody’s says “it’s premature to celebrate the end of the housing correction,” which is why it expects median home prices to decrease by 3.5% between the fourth quarters of 2023 and 2024, according to an updated forecast.

Andrew Lokenauth, owner of BeFluentInFinance: “Home prices will likely drop 5-10% nationally in 2024 as demand softens further. Affordability issues, economic uncertainty, and moderating investor activity will weigh on prices. Of course, the exact amount prices will reduce will depend on local market conditions and employment trends.”